How Americans bank is undergoing a lot of changes right now. Free checking as we know it is becoming an endangered species, people are doing a lot more of their banking online, and smartphones and prepaid debit cards are taking off. As we move towards 2013, with planning well underway at most banks, what are the megatrends that are impacting the way people bank?

Here is my take on the 5 key trends impacting consumers:

1. Banks' mobile and online banking features are more important than ever to your overall banking experience.

Not only are banks pushing them as a way to serve customers much more cheaply than they can in branches, but customers are getting much more comfortable with the technology, especially when it comes to mobile banking. You're definitely moving beyond the early adopters with mobile and online banking.

That means that having a welcoming, easy-to-use, powerful suite of technology products will be important criteria for the way customers choose banks in the future. And, if a consumer is one who is banking online or on their smartphone, they will probably look over a bank's technology offerings before signing up.

Number of Top 100 Banks Offering Mobile Services

|

| First Annapolis Group, 2012 Mobile Banking and Payments Study |

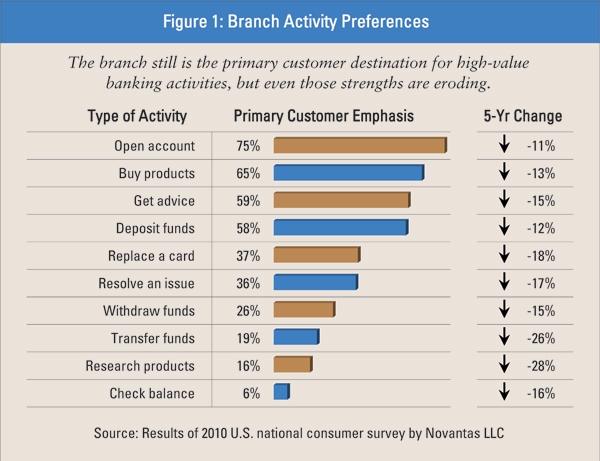

2. Banks' networks of branches will probably decline.

In the past, having a branch near their house or workplace was a big selling point for customers, but bricks and mortar have become less important because so much of customers' interaction with their banks now happens online. Branch transactions are going down. Mobile and online transactions are going up. The comfort level that people have with not having to deal with their bank face to face is becoming more and more clear.

While banks still look to branches to help with servicing customers and marketing their products, it's clear banks are looking to pare back their branch networks. The biggest reason why many banks haven't yet may come down to the real estate market.

Banks still have massive amounts of real estate, and there's no easy way to unload this burden in today's real estate market. In the meantime, many banks are looking for ways to transform traditional branches through the use of new digital technology.

3. Mobile wallets aren't ready to take off . . . yet.

Phone-based payments made at a store's register using a near-field communications chip like those incorporated in Google Wallet and Isis may never take off because they don't really give users anything they can't get with today's payment networks. As an industry, we get really excited about technology. But it's important that it's not technology for technology's sake, but that it actually brings value to the consumer. It's got to enhance the experience and go to a different level for people to change their behavior. Unfortunately, there hasn't been enough value from the consumer, merchant or banking perspective to help NFC (or today's mobile wallet solutions)

4. The next big thing is putting it all together.

There are some new mobile banking features on the way, such as the ability to use a mobile phone rather than a debit card to withdraw money from an ATM. But rather than adding a host of new features, the Holy Grail for banks right now is bringing all the features together in a usable package.

If you can put all your value cards in one location in your banking app along with remote deposit capture, personal finance management (PFM) capabilities, a non-card ATM accessibility tool, various budgeting tools AND combine relationships from multiple institutions (in one app) . . . that's going to make mobile banking more powerful."

5. Prepaid cards are going to give banks a run for their money.

The primary way many people use their banks these days is through using their debit card, online banking and mobile banking. That is not any different than some prepaid card providers are now offering customers. In fact, the new Bluebird product from Amex also offers remote deposit capture and potentially an integrated rewards program . . . for free.

I believe many banks underestimate the appeal of prepaid cards to a very high percentage of the public. While banks view this product as 'downmarket', consumers view this new combination of services as 'basic banking' . . . without the fees.

Digital technology is now taking over what was once solely owned by the big banks and traditional products. No longer do banks need to be represented by branches, large headquarters and massive marketing budgets. As Brett King says in the subtitle of his new book, Bank 3.0, banking is no longer somewhere you go, it is something you do'.

What do you think about these megatrends in banking from the consumer perspective? What else may change about the way your customers bank in the next couple of years?

No comments:

Post a Comment