At a time when retail banks are finding it difficult to achieve pre-recession levels of growth and profitability, the competition for wealth management business has never been more intense. But while increased marketing and significant monetary incentives are being used to lure customers, recent research indicates that organizational barriers remain that could hamper growth.

A just published Retirement Plans Trend Report conducted by the direct and digital monitoring firm Competiscan found that retirement rollover direct mail, electronic media and digital communication volumes increased during the second half of 2012 as did the value of offers used to entice customers. While many of these offers came from investment firms, more marketing was done by traditional banking organizations than in the past.

In 2012, Bank of America was one of the most aggressive wealth management marketers, cross-selling the services of their brokerage unit, Merrill Lynch to current higher value bank customers and prospects.

|

| Bank of America/Merrill Lynch Cross-Sell Mailing (December 2012) |

"Over the past couple years, we have seen more banks use targeted direct mail, email and digital communications to encourage 401(K) and other retirement rollovers from both customers and prospects", stated Richard Goldman, CEO and founder of Competiscan. "We have also seen the amount of incentive increase, indicating a greater focus on the affluent customer and the $200K+ rollover relationship."

Offers over the previous six months have ranged from $100 to as high as $600 for people who transfer higher amounts from existing plans. While some institutions have a sliding scale based on the amount transferred, others have a set offer with a minimum rollover balance requirement.

|

| ING 401(K) Rollover Direct Mail (December 2012) |

Direct mail isn't the only direct channel used to promote wealth management services, however. Institutions have used email and digital channels much more in the past 12 months according to the study from Competiscan. As can be expected, the majority of email communication is to existing customers, and includes a jump page link to more detailed information on the organization's website. Below is an example of email used by Capital One.

|

| Capital One Email (November 2012) |

Interestingly, in conjunction with more extensive marketing initiatives has come more extensive disclosures related to the products and offers. This is likely the result of the greater involvement of compliance that we are seeing in the development of all marketing communication over the past 18-24 months.

"Although the bonus rewards via direct mail and email continue to rise, we are observing an ever-growing amount of disclosures and caveats for reward redemption", stated Goldman from Competitscan. "The fine print seems to be growing proportionately with the proposed offers."

As with almost all financial services offerings, digital marketing is also increasing in use. Not only are banner ads being used within online banking sites, but banners are also being targeted to shoppers across the Internet. Below are examples of online banners used by Charles Schwab and Scottrade to generate leads. Both of these banners were used extensively on sites frequented by investors and used in conjunction with online search results.

|

| Charles Schwab Online Banner Ad |

|

| Scottrade Online Banner Ad |

Opportunity For Significant Growth

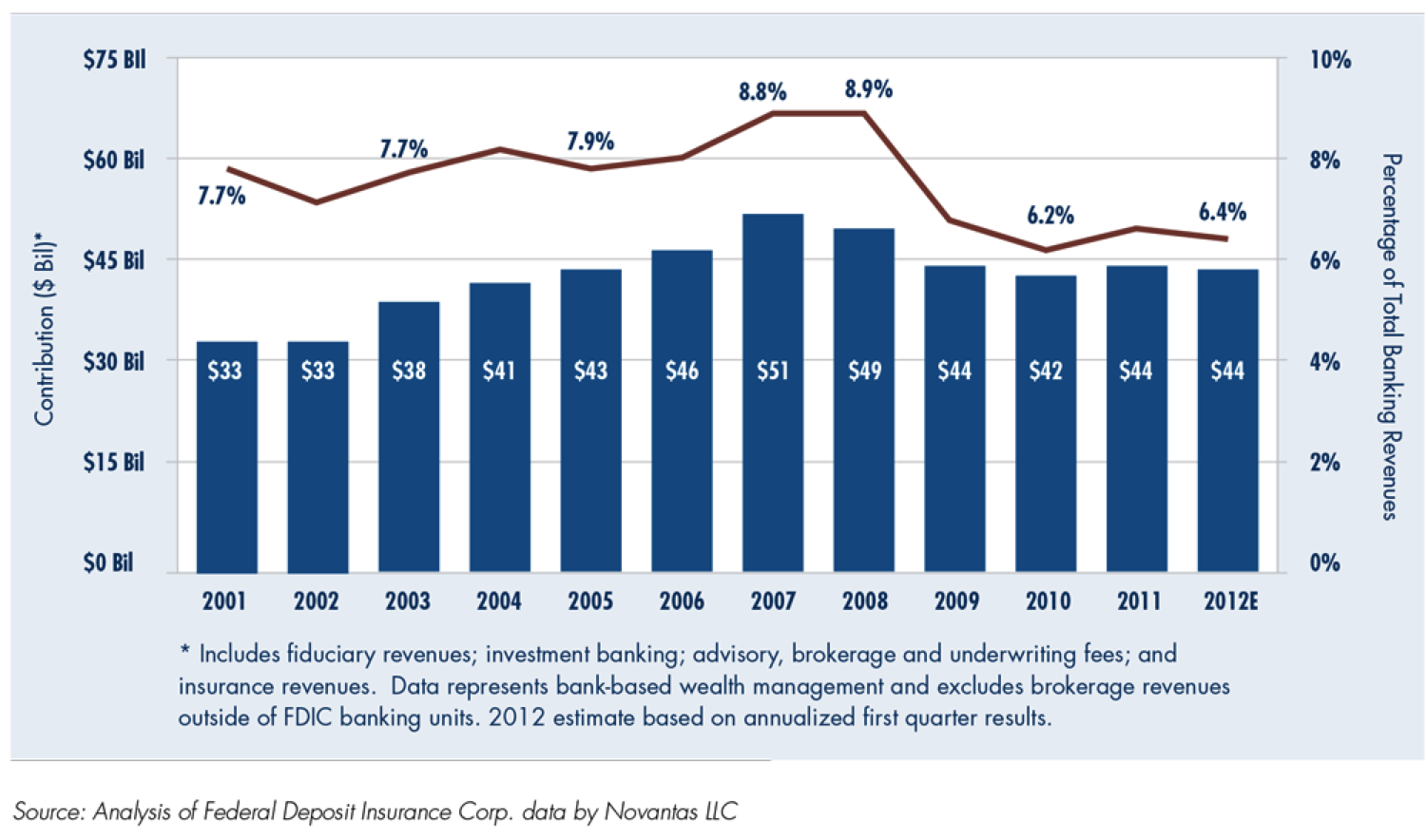

The increased marketing and incentives make sense for many banks given the search for additional revenues and fees. According to recent research from Novantas coordinated with the Bank Insurance and Securities Association (BISA), historical revenue contribution from wealth management has been modest compared to other lines of business, providing only 6 to 9 percent of revenues over the past several years.

The research entitled, Growing the Wealth Business in Retail Banking, included interviews with senior retail and wealth management executives from major banking firms across the country. Interestingly, despite increased marketing, the percentage contribution to revenues has actually decreased over the past couple years compared to the past as shown below.

Given the changing demographics of the retirement marketplace, the opportunity for growth is evident. According to Novantas, with existing relationships with baby boomers who are retiring, banks should be able to increase the revenue contribution from wealth management services to as high as 15 percent to 20 percent.

"As baby boomers prepare to retire and many households begin to search for longer term credible investment solutions, retail banks should increasingly view the wealth business as a strong alternative source of revenue," said Wayne Cutler, partner and head of the Wealth Management Practice at Novantas and author of the study.

To accomplish this, however, banks will need to substantially improve their wealth service cross-sell effectiveness which currently is only 3 to 5 percent at most large banks who took part in the research. The good news is that some participants in the study have already achieved a cross-sell penetration of between 10 to 15 percent of their retail base.

While marketing of wealth and retirement services has increased, it is not a top priority for all financial institutions based on the recently released 2013 State of Bank and Credit Union Marketing conducted by The Financial Brand. In fact, when more than 300 financial organizations were asked about the priority of marketing different products and services, retirement services was ranked #15 as shown below.

Marketing May Not Be Enough

Despite increased marketing that may get the consumer in the branch or visiting a jump page, the lack of senior management commitment to integrating the retail and wealth management businesses could be an impediment to optimal growth according to the Novantas study. In addition to a lack of top down commitment, challenges could include a lack of clearly defined strategy, insufficient product differentiation and the need for internal integration of the branch, call center and technological infrastructure.

The Novantas study found that several service models are being deployed by the largest institutions with varying results. While many firms believed a 'hub-and-spoke' approach to deploying wealth advisors was preferred, the success of this approach was contingent on strong relationships between the advisors and branch personnel, education of the front-facing staff and a strong referral discipline.

The good news is that many of the leading financial institutions have made wealth management and the affluent customer a top priority. Instead of parallel but disparate silos within the organization, many banks are trying to mesh the retail and wealth organizations to achieve an improved partnership. As this partnership improves, new products will be developed and a consistent sales model can be implemented across the organization.

As the sales model improves, the effectiveness of the direct channel communication will also improve since many leads and opportunities are currently lost due to organizational issues.

Additional Resources

Competiscan Q2 2012 Retirement Plans Trend Report - Available upon request by emailing richard@competiscan.com

The Mass Affluent: An Elusive Bank Target - Bank Marketing Strategy (November 2012)

The Mass Affluent: An Elusive Bank Target - Bank Marketing Strategy (November 2012)

Growing the Wealth Business In Retail Banking - Novantas (February, 2013)

2013 State of Bank and Credit Union Marketing - The Financial Brand (February 2013)

2013 State of Bank and Credit Union Marketing - The Financial Brand (February 2013)

We provide crypto marketing, crypto ads, do full-stack crypto promotion and provide the strategy for your crypto project. From A to Z.

ReplyDeletecrypto exchange marketing